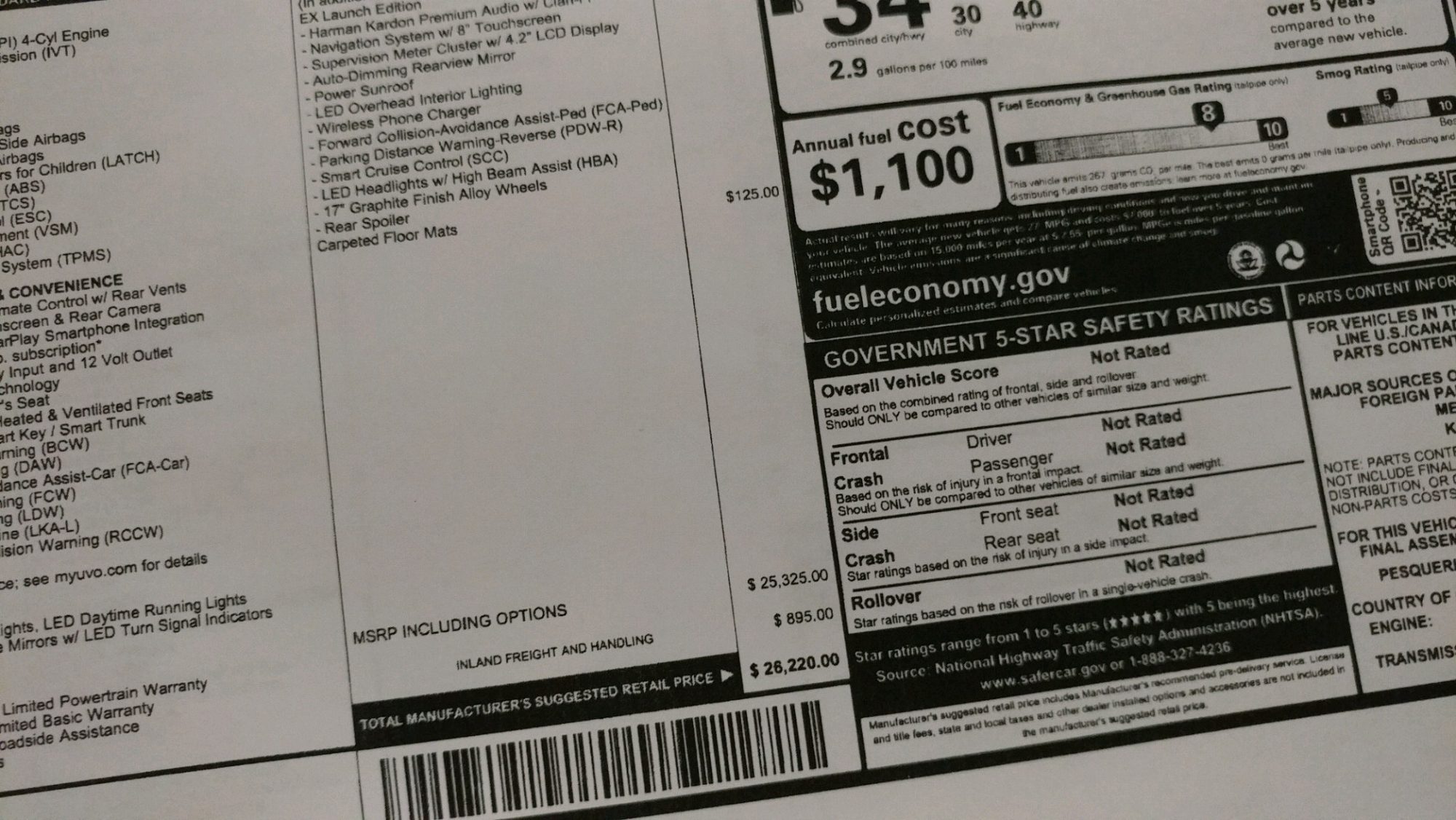

The top complaint heard by anyone in the automotive industry is about the price of a new car. Nearly every segment and every model has risen steadily to what appears to be a very large five-digit number. According to Edmunds research, new car prices have risen by 29 percent in the past decade (2009-2018).

The average car price is now over $36,000 and the average down payment for a new car is over $4,000.

The reasons for these increases are many, but many of them center around mandated requirements for vehicle safety and technology systems and on costs of manufacturing. Buyers are also fewer and further between, with fewer of the newer generation of buyers purchasing a new car (both by numbers and percentage) than there were 10 years ago. Yet the buyers that are out there are willing to shell out more to get more vehicle.

To go with larger car prices there are larger monthly payments. This explains why leasing is becoming more popular and why longer-term loans are also becoming more popular. The average buyer is now purchasing a car on a 69-month (6-year) loan at an average annual percentage rate of about 4.7 percent. After a down payment of over $4,000.

Where things get tricky is in average household incomes. Those have only gone up by an average of six percent. Today’s average new car costs about half of the annual income for today’s household (income versus sticker price). Interest rates are also up, averaging about a point and a quarter higher over that same period.

Similar changes are happening in the used car market, which has seen both book and trade-in values go up at a rate almost equal to the cost of new cars. This is likely due to demand increasing, as more buyers turn to the used market for a deal.

To compensate some, however, cars are now safer, more powerful, quieter, and more tech savvy than they were a decade ago. Also partially to blame, at least for interest rate increases and monthly payment boosts, are sub-prime loans (loans to those with scores under 621). Those types of loans have increased in both the used and new car markets over the past decade. So have loans with smaller than suggested down payments. This sub-prime lending has meant an increase in defaults as well, mostly in the demographics of buyers under the age of 30.

This pathway of increased prices, easier loans, and more costs follows closely with what culminated in the housing market crash of 2008. Could we be seeing something similar in automotive? It’s possible for sure.